Chapter 4 - Section 4.1Productivity of Workforce

In any financial institution, human resources form the backbone of operations, more so in microlending institutions (MLIs), which operate on a foot on street model. The frontline staff are crucial to MLIs in building client trust, ensuring repayment discipline, and supporting portfolio growth. The proper recruitment, training, and retention directly impact the efficiency and asset quality of the microfinance industry, making HR as vital as financial capital. However, while financial resources have received much attention, human resource development has often not been given due prominence. Many delinquency-related challenges stem from the staff practices shaped by their lack of understanding of the organizational mission, motivation, and client-centric approach. The challenge is further compounded as frontline staff, like their low-income clients, often have limited education and come from humble backgrounds and are lowly paid.

Operational Eminence of Micro Lending Institutions

4.1 Productivity of Workforce

4.1.1 Workforce in MLIs

In any financial institution, human resources form the backbone of operations, more so in microlending institutions (MLIs), which operate on a foot on street model. The frontline staff are crucial to MLIs in building client trust, ensuring repayment discipline, and supporting portfolio growth. The proper recruitment, training, and retention directly impact the efficiency and asset quality of the microfinance industry, making HR as vital as financial capital. However, while financial resources have received much attention, human resource development has often not been given due prominence. Many delinquency-related challenges stem from the staff practices shaped by their lack of understanding of the organizational mission, motivation, and client-centric approach. The challenge is further compounded as frontline staff, like their low-income clients, often have limited education and come from humble backgrounds and are lowly paid.

The microfinance industry has recently been struggling to find committed and skilled employees in an adequate number. In recent years, HR challenges have aggravated due to changes in work culture across industries, changes in expectations of the workforce, increased work opportunities, especially in urban setups in the form of e-commerce and gig economy. Reports say around 12 million people work in gig economy, comprising over 2% of the total workforce. However, microfinance has some advantages over gig employment. In microfinance, employment is generally more stable and institutionalised, with regular salaries, social security benefits, and opportunities for skill development. It enables individuals to contribute to community development and financial inclusion, providing a sense of purpose and long-term impact. While the rural workforce encompasses agriculture, informal sectors, and microfinance, employment in microfinance is likely a minimal share compared to these other sectors.

The microfinance employee base as of March 2025 is 3.29 lakhs, which is a 15% increase from the last year. The growth dropped to half from 33% during FY2023-24 to 15% in FY2024- 25. The total employee base of microfinance accounts for 0.06% of the total Workforce in India. The NBFC-MFI segment employs 77% of the total workforce, representing a 1% decrease from the last year.

1 https://www.livemint.com/money/personal-finance/indias-gig-economy-in-2025-growth-formalisation-and-financialinclusion-explained-11753438649777.html

2 Total labour force in India is 56.5 crores as per article: https://economictimes.indiatimes.com/budget-2024/economicsurvey-2024/economic-survey-2024-57-3-per-cent-of-the-total-workforce-self-employed-18-3-per-cent-working-as-unpaidworkers/articleshow/111920479.cms?from=mdr

Figure 4.1.1: Number of MLI staff – Yearly trend and MLI-category-wise Break-up

The Loan officers, who form the base of the organisational hierarchy of a typical microfinance organisation, are instrumental in expanding the outreach of microfinance and building goodwill with microfinance clients. Microfinance has always been a hightouch activity, with personal contact playing a crucial role in delivering financial services to low-income clients. Human relationships and values such as trust and empathy are essential in determining the growth and sustainability of a Microfinance Institution. The MLIs’ frontline staff—the loan officers and other field staff—must uphold the values and maintain relationships with their clients, being the face for the MLIs to their borrowers. The Loan officers hold a critical position in influencing clients’ experiences with access to credit and their engagement with an MLI.

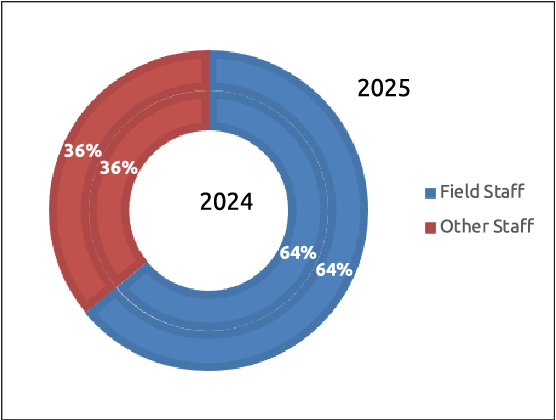

At the end of the last financial year, there were 2.09 lakhs field staff, which comprise 64% of the total staff. This ratio is unchanged from the last year. However, in terms of absolute numbers, the field staff has increased by 14%.

Figure 4.1.2: Distribution of staff in the last two years

Although microfinance borrowers are predominantly catering to women borrowers, the number being more than 95%, the share of women staff to the total staff in microfinance is very less. The primary reasons for the low share of women employees may be due to the rigours of microfinance operations, which include longer hours of operation, Societal restrictions on women’s mobility, concern for their safety, and lack of awareness regarding such work opportunities. Moreover, at the macro level, the participation rate of the female labour force in India at 35.6% is lower than that of men (77.5%) as per 2023-24 data3 . As of FY 2024-25, the microfinance industry employs a total of 30,725 female employees, of which 54% are field staff. However, this accounts for only 9% of the total employee base in the Microfinance Industry, which has been showing a steady declining trend from 2014 onwards, as can be seen from table 4.1.1.

Table 4.1.1: Year-wise staff strength in MLIs and share of women staff

| Year | Total Staff (in lakh) | Women Staff (in lakh) | % of Women Staff to Total Staff |

|---|---|---|---|

| 2014 | 0.80 | 0.15 | 19% |

| 2015 | 0.95 | 0.15 | 16% |

| 2016 | 1.03 | 0.16 | 15% |

| 2017 | 0.90 | 0.11 | 12% |

| 2018 | 1.11 | 0.13 | 12% |

| 2019 | 1.38 | 0.16 | 12% |

| 2020 | 1.52 | 0.17 | 11% |

| 2021 | 1.61 | 0.17 | 10% |

| 2022 | 1.95 | 0.25 | 13% |

| 2023 | 2.16 | 0.26 | 12% |

| 2024 | 2.87 | 0.31 | 11% |

| 2025 | 3.29 | 0.31 | 9% |

There are many challenges that an MLI faces in recruiting and retaining the right kind of human resources, such as finding qualified and motivated candidates, skilling them and managing their motivational level, which can withstand the competitive demands of other sectors. Over the last financial year, the sector recruited 2.06 lakh new staff, representing a 22% increase from the previous year. The NBFC-MFIs recruited 77% of the new staff, and 77% of these staff members were placed in the very large (portfolio above ₹2,000 cr).

Figure 4.1.3: New Staff Recruitment and their break-up based on Legal Form and Size

3 Periodic Labour Force Survey (PLFS) Annual Report [July 2023 – June 2024].

Attrition of staff has become a significant concern for the MLIs’ operations. This is more so in recent days, especially after Covid pandemic, the movement of staff has been seen much sharper. In some cases, attrition is so high that the entire frontline staff is replaced in one or two years. Attrition is most commonly observed among entry-level staff, typically within the first three months. SaDhan’s internal study on the reasons behind high attrition reveals some key reasons, such as high work pressure and long working hours, both of which are attributed to increased delinquency in the sector. These issues, combined with the new opportunities that have emerged over the last few years, such as the gig economy and a shift in work culture worldwide, have fuelled the increase in attrition for the sector. According to a recent report by The Economic Times, the banking sector has witnessed a 103% attrition rate, while the NBFC segment has posted a 77% attrition rate7 as of end of December 2024. During the financial year 2024-25, the sector observed an overall attrition rate of around 52%.

Table 4.1.2: Staff Attrition across different categories during FY 2024-25

| Categories of institutions based on legal status and size of business | No. of staff at the beginning of the year (i.e., April’24) | No. of staff who left/dropped during the year | No. of new Staff recruited during the year | No. of staff at the end of the year (i.e., March 25) |

|---|---|---|---|---|

| Staff Attrition across Legal Form of MLIs | ||||

| NBFC-MFIs | 2,22,186 | 1,27,326 | 1,58,827 | 2,53,687 |

| NBFCs | 27,303 | 14,499 | 29,580 | 42,384 |

| Pvt. & Pub Ltd. Coms | 21,734 | 16,572 | 16,341 | 21,503 |

| Sec. 8 Coms | 1,423 | 483 | 534 | 1,474 |

| Other NGO-MFIs | 10,546 | 918 | 793 | 10,421 |

| Total | 2,83,192 | 1,59,798 | 2,06,075 | 3,29,469 |

| Staff Attrition across Size of MLIs | ||||

| ≤100 Cr. | 7,311 | 3,011 | 4,068 | 8,368 |

| ₹100 Cr.–₹500 Cr. | 22,181 | 13,926 | 14,637 | 22,892 |

| ₹500 Cr.–₹2000 Cr. | 37,092 | 23,999 | 28,654 | 41,747 |

| ≥2000 Cr. | 2,16,608 | 1,18,862 | 1,58,716 | 2,56,462 |

| Total | 2,83,192 | 1,59,798 | 2,06,075 | 3,29,469 |

There is an employee bureau set up by Equifax India in 2017 for the microfinance industry, which is quite a unique initiative. This is part of Equifax’s India Workforce Solutions (IWS) offering, allows MFIs to access real-time, non-finance employment data to improve hiring quality and prevent fraudulent activities among their large, mobile, and primarily field-level workforce. Around 77% reported MLIs (100 out of 130) are participating in the bureau by sharing information and using it for background checks during staff onboarding.

4 https://economictimes.indiatimes.com/jobs/hr-policies-trends attrition-rate-surges-among-junior-staff-in-private-banks/ articleshow/117992846.cms?from=mdr

4.1.2 Staff Productivity

Active Borrowers per Credit Officer (ABCO) and Active Borrowers per staff (ABS)

Over the last two decades, the sector has undergone an operational shift, as most microlending institutions (MLIs) have transitioned from paper-based operations to digital by implementing Management Information System (MIS) and core banking solutions (CBS). Many of the MFIs have also adopted digitalisation of field service and complementary back-office operations through Digital Field Applications (DFAs), which facilitate onboarding, loan applications, account opening, and transactions in the field. Some of the MLIs have also moved into the next phase of digitization by involving AI and agent AI tools. Digitisation of the process has clear value for MLI as it increases staff productivity and improves the end customers’ experience. Despite these developments, the involvement of human resources is still important in various microfinance processes. Hence the enhancing the productivity of the human resource is important in improving the profitability of the operations. An efficient and productive staff will contribute to the growth of the MLIs

The primary indicator for assessing staff performance is to understand the number of borrowers each loan officer is responsible for handling. However, even with the increased inclination towards innovative technology, the Average Borrower per Credit Officer (ABCO) (ABCO) is moving downward. There could be several reasons why MLIs are unable to fully leverage technology. Some of these reasons are an increase in delinquency, which forces loan officers to spend more time on each repayment collection, stricter underwriting norms, which have reduced the active borrower base over the last year, an increase in rejection rate of borrowers’ applications, forcing them to spend more time on sourcing, which leads to a decrease in borrowers per loan officer.

During the financial year, we see a change in the composition of MLIs under each bucket of ABCO and Average Borrower per Staff (ABS). For ABS, a significant increase in the 100- 200 bucket is seen. In the case of ABCO, a substantial increase is observed in the lowest two buckets, i.e., the categories ‘less than 200 ‘and ‘200-300’ buckets. The share of MLIs under the ‘100-200’ bucket for Looks different font. Please correct it.

Over the financial year 2024-25, the ABCO decreased by 21%, marking the lowest ABCO recorded over the last five years. Similarly, ABS also experienced a significant decrease, from 243 to 190, resulting in a 22% drop.

Figure 4.1.4 Distribution of MLIs based on clients served per Staff and Credit Officer

Figure 4.1.5: Trends of ABCO Across MLIs and break-up of 2025 in terms of Legal Form and Size

Figure 4.1.6: Trends of ABS Across MLIs and break-up of 2025 in terms of Legal Form and Size

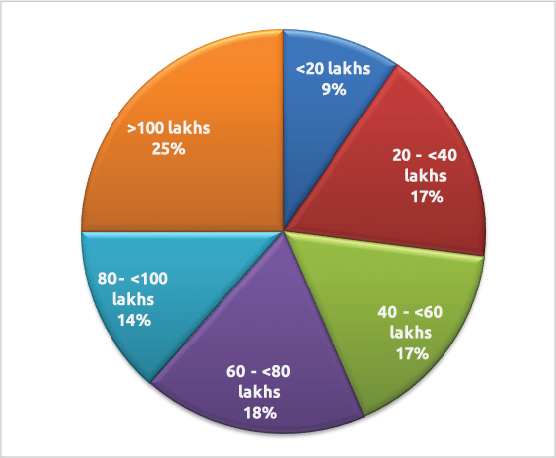

4.1.3 Distribution of MLIs Based on Loan Portfolio per Credit Officer

The portfolio outstanding under each loan officer is also a key indicator of staff productivity. It shows the workload and capacity of individual loan officers. The current year recorded an overall ₹1.14 crore portfolio handled by each loan officer. The distribution of MLIs across each bucket of the portfolio per loan officer has remained almost unchanged compared to last year. However, we see a decrease in the ‘>100 lakhs’ category from 74 to 50 and a slight increase in the ‘20- 40 lakhs’ category from 24 to 35 MLIs.

Figure 4.1.7: Distribution of MLIs Based on Loan Portfolio per Credit Officer

Conclusion

The workforce remains the cornerstone of operational excellence in microfinance institutions. Despite steady growth in employee numbers, the sector continues to grapple with high attrition, low female participation, and the challenge of balancing field-level demands with employee motivation and retention. Loan officers, who are central to client engagement and repayment discipline, face increasing workload pressures amid rising delinquencies. While digitisation has improved processes, productivity indicators such as ABCO and ABS have declined, reflecting the strain on field operations.

These trends underscore the urgent need for stronger human resource strategies—focused on recruitment, retention, capacity building, and gender inclusivity—alongside effective use of technology to enhance efficiency. For MLIs, sustaining growth and maintaining portfolio quality will depend as much on strengthening human capital as on financial capital.