Chapter 4 - Section 4.3Income and Expenditure Analysis

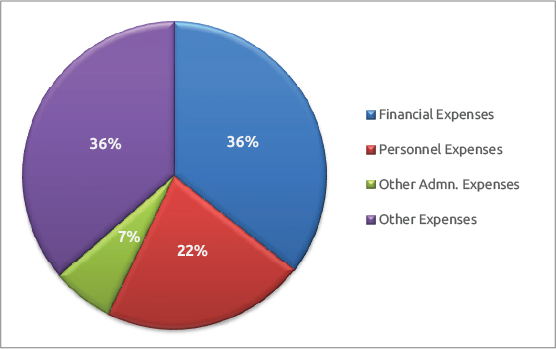

Maintaining sound financial health is essential for the long-term sustainability of financial institutions, particularly microlending institutions (MLIs). Rising delinquencies pose a significant threat, resulting in substantial financial losses and multiple structural challenges. Higher credit costs translate into heavier provisioning burdens, while unpaid loans reduce net interest income and restrict lending capacity, directly curbing growth and profitability. At the same time, intensified recovery and monitoring efforts drive up operational expenses, further straining margins. Persistently high delinquency levels can also erode the confidence of lenders and investors, jeopardizing access to fresh capital and bank funding—risks that are especially pronounced for smaller MFIs. component contributes to 29% of the total expenses this year. The same trend is prevalent across various size segments. The trend in the first quarter of the FY 2025-26 also indicates a similar trend. It appears that this trend may persist in the first half of FY 2025-26

Chapter 4: Section III

Income and Expenditure Analysis

aintaining sound financial health is essential for the long-term sustainability of financial institutions, particularly microlending institutions (MLIs). Rising delinquencies pose a significant threat, resulting in substantial financial losses and multiple structural challenges. Higher credit costs translate into heavier provisioning burdens, while unpaid loans reduce net interest income and restrict lending capacity, directly curbing growth and profitability. At the same time, intensified recovery and monitoring efforts drive up operational expenses, further straining margins. Persistently high delinquency levels can also erode the confidence of lenders and investors, jeopardizing access to fresh capital and bank funding—risks that are especially pronounced for smaller MFIs. component contributes to 22% of the total expenses this year. The same trend is prevalent across various size segments. The trend in the first quarter of the FY 2025-26 also indicates a similar trend. It appears that this trend may persist in the first half of FY 2025-26

Figure 4.3.1: Breakdown of expenses under various categories by MLIs

4.3.1 Expenditure Analysis

Since MLIs in India are not permitted to take deposits, the microfinance model is heavily dependent on raising debt funds from Banks for on-lending. Therefore, the significant component of MLIs’ cost structure is financial cost. The finance cost is followed by personnel (human resources) cost, as the model is heavily labour-intensive due to the door-todoor collection method. However, for the FY 2024-25, this composition changed due to an increase in Loan Loss Provision Expenses. This An analysis of different legal forms indicates a change in the composition of expenses, especially in the case of ‘Pvt & Pub Ltd Coms. For this segment, the most significant expense is personnel cost. These types of MLIs only operate as Business Correspondents as per the guidelines shared by the Ministry of Corporate Affairs, and hence, there is no financial cost, as they incur little cost to raise funds. Interestingly, a similar trend can be observed in the case of Section 8 companies, too.

Figure 4.3.2: Break up of expenses by Indian MLIs based on portfolio size and legal form

4.3.1.i Operating Cost1

Operating costs play a critical role in shaping the pricing structure of MLIs, as they directly influence the interest rates and fees charged to borrowers. Since these institutions function on narrow margins, any increase in cost is often transferred to clients, raising their repayment burden and affecting institutional self-reliance. A lower operating cost ratio signals higher efficiency, enabling MLIs to provide affordable loans, improve competitiveness, and extend outreach. In contrast, rising costs diminish lending capacity, squeeze profitability, and risk, pushing institutions toward donor dependence. Over the past five years, operating costs hovered around 6-7%, largely driven by elevated delinquencies, staff attrition, and efforts to expand into underserved markets.

Figure 4.3.3: Trends of Operating Cost across MLI Categories

1 Define as (Personnel Cost including incentive + Travel Cost + Admin Cost + Group Dev. Cost/Training Cost + Depreciation + Any Others)/Average Portfolio Outstanding.

4.3.1.ii Finance Cost2

Finance costs are equally decisive, as they determine both lending rates and the extent of outreach. Persistently high finance costs leave MLIs with limited flexibility, often compelling them to raise interest rates, which reduces affordability and can also strain repayment behaviour. In contrast, periods of declining finance costs have allowed institutions to price loans more competitively, strengthen repayment discipline, and broaden their client base. Lower borrowing costs have also supported better margins, enabling MLIs to build reserves and reinvest in growth. Conversely, elevated finance costs have curtailed expansion, undermined profitability, and increased dependence on subsidies or external donor support. Between 2018 and 2025, managing finance costs has remained central to balancing financial sustainability with client affordability, underscoring its role as a cornerstone of microfinance operations.

Figure 4.3.4: Trends of Finance Cost across MLI Categories

4.3.1.iii Trends of OperatingCost and Finance Cost

Finance costs and operating costs have consistently played a significant role in determining portfolio quality, as measured by PAR exceeding 30 days. High costs increase the pressure on MLIs to charge higher interest rates and fees, which in turn reduces borrower repayment capacity and raises delinquency risk. Conversely, when costs have been better controlled, institutions have been able to maintain more affordable lending terms and support the health of their portfolios. In 2021– 22, despite moderating finance costs, high operating costs and overall expense pressures coincided with the covid pandemic, made a surge in PAR to above 7%, indicating weakened borrower repayment capacity. In 2023–24, both costs stabilized, and PAR dropped to below 3%, highlighting how efficiency gains supported repayment discipline and portfolio health. By 2025, rising finance costs (11.5%) and operating costs (7.09%) again pushed PAR up to 7.52%. This demonstrates that cost control is essential not just for profitability but also for credit risk management.

2 Define as the Total expense incurred for acquiring funds /Average Outstanding Borrowings

4.3.1.iv Cost per borrower

An analysis of MLIs’ income and cost structure from the perspective of cost and income per active borrower can help to understand the sustainability of the income-cost structure of the MLI. For Micro Lending Institutions (MLIs), cost per borrower is a critical indicator of operational efficiency, sustainability, and ability to serve clients effectively. A lower cost per borrower suggests the MLI is efficient in its operations and can potentially offer lower interest rates or greater outreach to the poor. Conversely, a high cost per borrower may signal inefficiencies that hinder expansion, require higher interest rates to remain viable, or limit financial inclusion

The data shows that MLIs face a narrow margin3 between expenses4 (₹5,861) and income5 (₹5,780) per borrower, reflecting overall financial strain. Expenses per borrower vary widely across institutions, shaping efficiency and risk. NBFC-MFIs incur the highest costs (₹7,628), reflecting fieldintensive operations and compliance needs, but such high expenses pressure margins and borrower affordability. NBFCs (₹1,483) and Section 8 companies (₹1,261) show far leaner models, indicating stronger cost efficiency. Smaller MFIs (<₹100 cr) manage relatively low expenses (₹4,758), while mid-sized and large MFIs see rising costs above ₹6,000 per borrower, suggesting diseconomies of scale. Overall, higher expenses often result in thinner surpluses, repayment stress, and increased credit risk.

Figure 4.3.5 Expenses per borrower under various categories

4.3.2 Income Analysis

The primary source of income for MLIs is the interest earned on their loan portfolios, supplemented by various fees and commissions, including service charges, processing fees, and revenues from non-credit products. Profitability depends on the ability to generate sufficient revenue to cover both operating and financial costs, with interest, fees, and commissions historically forming the bulk of financial income. However, this heavy reliance on loan-related revenue poses a challenge: any increase in expenses can be offset only in two ways—either by raising interest rates, fees, or commissions (which directly increases the burden on borrowers), or by incurring losses. Consequently, understanding and analysing the revenue streams of MLIs is crucial for institutions aiming to strengthen profitability, diversify income sources, and reduce overdependence on borrowers. The total revenue generated by MLIs during FY2024-25 is ₹36,221 crores, out of which 81% is from interest income from the loan portfolio. The total income has increased by 10% from the income of FY2023-24, which is lower than the growth rate of FY2023-24 (18%).

3 Margin here refers to the difference between expenses per borrower and income per borrower.

4 Calculated as aggregated total expenses (finance, human resource, admin and other expenses) of all MLI divided by the total active borrower.

5 Calculated as aggregated total income of all MLIs divided by total active borrowers.

Figure 4.3.6: Break-up of Income

4.3.2.i Yield on Loan Portfolio

Yield is a vital indicator in microfinance as it reflects both sustainability and efficiency. Since MLIs provide small, collateral-free loans to low-income clients, operating costs and risks are high. Yield ensures that institutions earn sufficient interest and fees to cover expenses, absorb credit risks, and maintain investor confidence. It also serves as a benchmark for efficiency, highlighting whether operations are sustainable and efficient. However, yields must strike a balance between financial viability and client affordability, as excessively high rates undermine the social mission of microfinance Thus, yield is central to ensuring both growth and responsible financial inclusion. Historically, over the last two decades, yield has been mostly between 20-22%.

The industry experienced its lowest yield between 2020 and 2022, a result of the pandemic’s shock. Following two years, i.e., 2022-2023 and 2023-24, the yield returned to the pre-COVID level. However, in FY2024- 25, it again fell behind. This highlights the challenges faced by the MLIs during the year (2024-25) in terms of external shocks such as climate change, loan waiver rumours, and internal issues like repayment stress, higher attrition, etc.

Figure 4.3.7: Yield Trend of MLIs

A similar trend of lower yield compared to the previous year (FY2023-24) prevails for different legal types and sizes of MLIs.

Figure 4.3.8: Yield on Portfolio across MLIs

4.3.3 Margin

The Financial Margin is calculated as the difference between the Yield and the cost of borrowing. The spread between yield and finance cost covers the operational cost, including loan loss provisions, other expenses and net profit margin. The margin covers the operating cost and the profit margin of the MLI. The weighted average Margin in FY2024- 25 stands at 7.99%, which is very small for an industry like microfinance, where the operational cost and risk cost tend to be high.

Figure 4.3.9: Yield, Cost and Margin of MLIs – size-wise based on weighted average values

Conclusion

The analysis of income and expenditure highlights the fragile balance that microlending institutions must maintain between financial sustainability and social outreach. Rising delinquencies, high finance costs, and escalating operating expenses have intensified pressure on margins, leaving institutions with little room to absorb shocks. The cost per borrower remains elevated for many categories, eroding efficiency and threatening borrower affordability, while income streams remain heavily concentrated in interest earnings, underscoring the vulnerability to repayment stress. The fluctuating yield trends and shrinking margins further emphasise the need for stronger cost controls, income diversification, and operational innovations. Ultimately, the long-term resilience of MLIs depends on their ability to optimise expenses, stabilise income, and maintain affordable credit access, ensuring both institutional sustainability and meaningful financial inclusion.